A Guide to Private Credit in 2025

A Guide to Private Credit in 2025

It’s undeniable: private credit is having a moment. After years remaining on the sidelines as a last-resort funding option, private credit has emerged as a crucial component of private equity strategies. As US Secretary of the Treasury Scott Bessent noted in a recent podcast interview, private credit is an “exciting” option that “meets businesses where they are.” As increasing regulations have tightened traditional lending options, private credit offers both stability and opportunity for PE firms looking to maximize returns in challenging economic conditions.

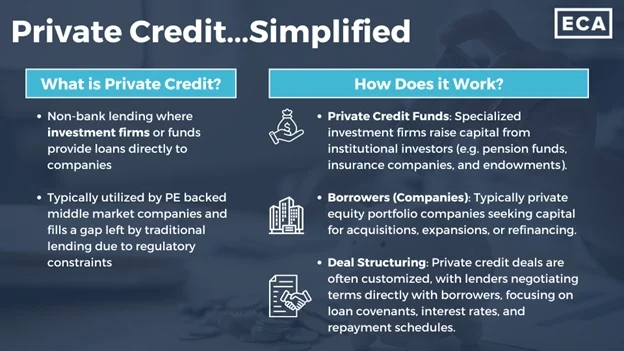

How Does Private Credit Work?

Market Growth and Current Trends

Key Drivers of Private Credit Expansion

Private Credit Strategies Within PE

Integration of Private Credit and Private Equity

Challenges and Risk Considerations

Looking Forward

Conclusion

How Does Private Credit Work?

Have a role you'd like to discuss?

Looking to expand your team?

Market Growth and Current Trends

Private credit has experienced remarkable growth over the past decade, reaching unprecedented levels in 2025. As S&P Global Ratings notes, “Private credit’s growth won’t be slowing down anytime soon” with recent rate cuts providing relief for borrowers through lower funding costs. The market now represents a significant portion of alternative asset allocation, with institutional investors increasingly favoring these strategies for their portfolio diversification.

According to Wellington, “The growth of private credit should persist in 2025, continuing a decade-plus trend. The asset class’s steady expansion suggests a growing recognition of the role it can play as both a complement and diversifier to traditional credit investments.” This middle-ground approach has been particularly attractive during recent market fluctuations, where predictable income streams offer security amidst uncertainty.

Key Drivers of Private Credit Expansion

Several factors continue to drive the expansion of private credit within PE operations:

First, regulatory pressures on traditional banks have created a financing gap that private credit providers now fill. Banking regulations implemented post-financial crisis continue to limit traditional lenders’ capacity to finance certain transactions, particularly those involving higher leverage or complex structures.

Second, the current interest rate environment, while stabilizing compared to the volatility of 2022-2023, still presents challenges for traditional fixed income investments. As MSCI Research points out, “Private-credit funds posted strong returns in 2024 as the strategy experienced its first real interest-rate cycle, but the winds may be shifting heading into 2025,” as index rates remain significantly elevated from pre-2022 levels.

Third, the growth of specialized financing needs has accelerated. As Dechert LLP reports, “Private credit has rapidly expanded from its direct lending roots into new areas, including an ever-diversifying range of asset-backed finance structures, with bespoke deals shaping the market.” Middle-market companies in particular require customized financing solutions that traditional banking often cannot provide efficiently.

Private Credit Strategies Within PE

PE firms are deploying private credit through various strategies, each tailored to specific market segments and risk profiles:

Direct Lending remains the cornerstone of private credit strategies, with PE firms providing senior secured loans directly to middle-market companies. These loans typically feature floating rates, providing a hedge against inflation while offering strong covenant protection.

Distressed Debt strategies have evolved significantly in 2025. Rather than focusing solely on deeply troubled companies, PE firms now implement more nuanced approaches to companies facing temporary challenges but with fundamentally sound business models.

Specialized Financing Solutions have gained prominence, including asset-based lending, royalty financing, and various forms of structured credit. According to Moonfare, private credit’s flexibility continues to serve it well even as interest rates fall, as rates “will likely remain higher than many businesses had become accustomed to before the pandemic.”

Private Credit Secondaries have emerged as an increasingly important market segment, with McKinsey noting that “Secondaries transaction value rose 45 percent to an all-time high of $162 billion last year,” providing critical liquidity for limited partners.

Integration of Private Credit and Private Equity

The convergence of private credit and private equity continues to reshape investment strategies. As EY reports, “Already, private credit funds have amassed US$1.5t in assets under management (AUM), a figure expected to grow to nearly US$3t over the next five years.” Many PE firms now maintain dedicated credit arms, allowing them to provide comprehensive capital solutions across the capital structure.

This integration creates strategic advantages:

- The ability to offer “one-stop” financing solutions to portfolio companies

- Enhanced due diligence capabilities from multiple perspectives

- Flexibility to pivot between equity and debt positions based on market conditions

- Extended relationships with portfolio companies through various financing stages

Challenges and Risk Considerations

Despite its growth, private credit within PE faces several challenges:

Increased competition has compressed yields in certain market segments, particularly in larger, more established deals. Morgan Stanley Investment Management notes they are focusing on “maintaining a portfolio that is diversified across sectors” while avoiding “deeply cyclical capital-intensive businesses” in the current economic environment. This competitive pressure has pushed some firms toward riskier segments of the market in search of higher returns.

Liquidity risks remain a consideration, as private credit investments typically involve longer holding periods than public market alternatives. However, the increase in PE capital in recent years may allay these fears. As McKinsey reports, “Global private equity dry powder decreased 11 percent (to $2.1 trillion) between the first half of 2023 and the first half of 2024.”

At the same time, default risk assessment has become more complex in the current economic environment. MSCI warns that “some borrowers have begun to founder under now-burdensome debt-service costs” despite the benefits of recent rate cuts, creating a potentially choppy environment for private credit in the year to come.

Looking Forward

The remainder of 2025 presents both opportunities and challenges for private credit in PE. As Cherry Bekaert reports, “Private equity heads into 2025 with a degree of optimism, as both macroeconomic and regulatory conditions are generally expected to be more favorable for dealmaking.”

Further integration between private credit and private equity functions will likely continue, with more firms developing comprehensive capital solutions approaches. Technological innovation will remain a differentiator, with the most successful firms leveraging advanced analytics to identify opportunities others miss. Finally, regulatory developments will require ongoing attention, as changes in banking regulations and tax policies could significantly impact private credit strategies.

Conclusion

As we’ve seen, private credit has firmly established itself as a critical component of private equity strategies in 2025—it’s no coincidence the Secretary Treasury is talking it up as a “dynamic” alternative to traditional lending.

For PE firms, developing robust private credit capabilities is no longer optional but essential for maintaining competitive positions in an increasingly complex marketplace. Those firms that successfully integrate private credit strategies with traditional PE approaches, while effectively leveraging technology, will be best positioned to navigate the opportunities and challenges that lie ahead.

As the line between private credit and private equity continues to blur, the most successful firms will be those that can seamlessly move between different positions in the capital structure, providing comprehensive solutions to portfolio companies while generating attractive risk-adjusted returns for investors.

Ken Kanara is a Managing Partner at ECA Partners. He can be reached at [email protected].